![[HERO] Voluntary vs. Core Benefits: A Plain-Language Guide on How They Work (And Why It Matters)](https://cdn.marblism.com/MbwLTyU9HCr.webp)

If you’ve ever sat through a benefits meeting and walked away more confused than when you started, you’re not alone. The terms “core benefits” and “voluntary benefits” get tossed around like everyone just knows what they mean. Spoiler: most people don’t.

Here’s the thing, understanding the difference between these two types of benefits isn’t just insurance-speak. It’s the key to building a benefits package that actually works for your team without breaking your budget. Let’s clear up the confusion once and for all.

Core Benefits: The Non-Negotiables

Think of core benefits as the foundation of your benefits house. These are the must-haves, the coverage you’re legally required to offer (or the basics that make you a competitive employer).

Core benefits typically include:

- Health insurance (medical coverage)

- Retirement plans (like a 401(k))

- Paid time off (vacation, sick leave)

- Workers’ compensation

- Unemployment insurance

Depending on your state and company size, you might also be required to offer disability insurance or paid family leave. The big thing to remember? You, the employer, foot most (or all) of the bill for core benefits.

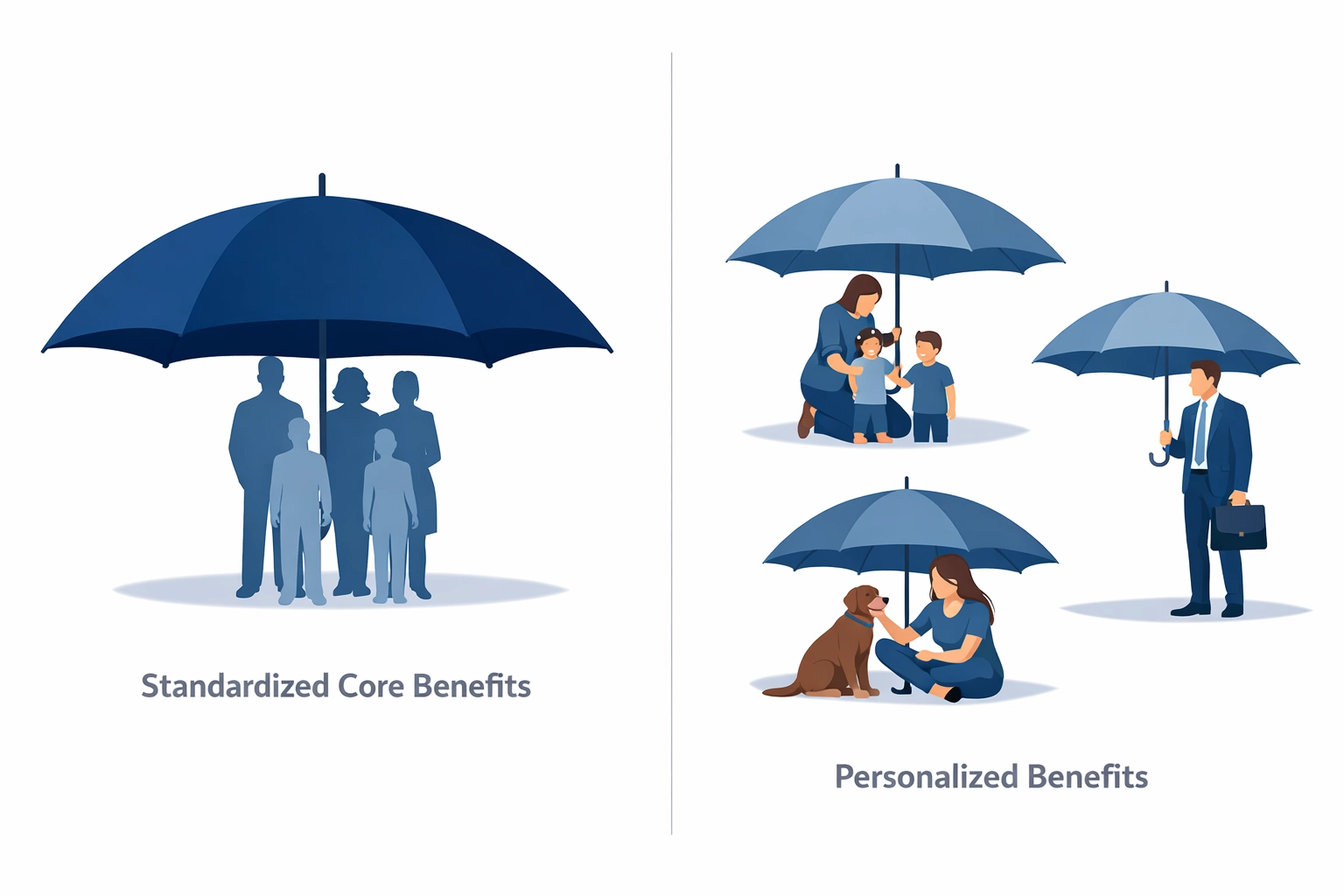

These benefits are standardized across your workforce. Everyone gets access to the same health plan options, the same retirement match, the same PTO policy. They’re designed to cover the basics, keeping your team healthy, financially stable, and protected.

Voluntary Benefits: The Personal Choices

Now here’s where it gets interesting. Voluntary benefits are the optional add-ons your employees can choose based on their own needs and life situations. And here’s the kicker: employees pay for them through payroll deductions.

That means zero cost to you as the employer, but your team still gets access to group rates they’d never find on their own.

Common voluntary benefits include:

- Dental and vision insurance

- Life insurance (supplemental coverage beyond any employer-paid policy)

- Accident insurance

- Critical illness insurance

- Hospital indemnity insurance

- Short-term disability

- Pet insurance

- Identity theft protection

- Legal services plans

Unlike core benefits, voluntary coverage is deeply personal. One employee might prioritize extra life insurance because they have young kids. Another might choose accident coverage because they’re an avid mountain biker. Someone else might opt for pet insurance because their dog is basically their child.

The beauty of voluntary benefits? They’re portable. If an employee leaves your company, they can often take these policies with them, no gaps in coverage, no scrambling to find a new plan.

So What’s the Real Difference?

Let’s break this down in the simplest terms possible:

Core Benefits are the table stakes. You have to offer them (or you should if you want to attract talent). You pay for them. Everyone gets the same options.

Voluntary Benefits are the buffet. Employees pick what they want. They pay for them. You provide access to great group rates and make enrollment easy through payroll deduction.

Here’s a quick side-by-side:

Why Employers Should Care

I get it, you’re already juggling a million things. Why add more benefits to the mix if they don’t cost you anything directly?

Here’s why: voluntary benefits are one of the smartest, most budget-friendly ways to compete for talent.

When you offer voluntary benefits, you’re telling your team, “We see you as individuals. We know one health plan doesn’t fit everyone’s life.” That message matters, especially in tight labor markets or industries where turnover is costly.

Plus, offering voluntary benefits through your workplace gives employees access to group pricing. That’s a real, tangible value-add. Your employees aren’t paying retail rates for coverage. They’re getting better deals because they’re part of your group.

And let’s be honest: recruiting and retention are expensive. If offering voluntary benefits helps you keep good people longer, that’s money saved on hiring, onboarding, and training.

Why Employees Should Care

If you’re an employee reading this (or an HR leader trying to explain this to your team), here’s the bottom line: core benefits alone don’t cover everything life throws at you.

Health insurance is great, until you’re hit with a $5,000 deductible after an unexpected ER visit. That’s where hospital indemnity insurance steps in, paying you cash to cover those out-of-pocket costs.

Your employer might offer basic life insurance (often one or two times your salary), but is that enough to protect your family if something happens to you? Voluntary life insurance lets you buy more coverage at group rates, tailored to your actual needs.

Critical illness insurance pays a lump sum if you’re diagnosed with something like cancer, a heart attack, or a stroke. That cash can cover anything, medical bills, mortgage payments, lost income while you recover. Your traditional health plan doesn’t do that.

The point? Voluntary benefits fill the gaps. They give you a financial safety net for the things core benefits simply don’t cover.

The Personal Touch: Why 1-to-1 Counseling Matters

Here’s where a lot of companies drop the ball: they offer voluntary benefits, but employees have no clue what they are, how they work, or whether they actually need them.

That’s why one-on-one benefits counseling makes all the difference. When employees sit down with someone who can explain the options in plain English, no jargon, no pressure, they make smarter decisions.

We’ve seen it time and time again: when employees understand what they’re buying and why it matters, enrollment rates skyrocket. And more importantly, people walk away feeling confident they’ve built the right safety net for their family.

That personal conversation turns confusing insurance-speak into “Oh, I get it now. This actually makes sense for me.”

Putting It All Together

Core benefits and voluntary benefits aren’t competitors: they’re teammates. Core benefits give everyone the essentials. Voluntary benefits let people personalize their coverage based on where they are in life.

For employers, it’s a win-win: you offer a richer benefits experience without a major budget hit. For employees, it’s peace of mind knowing they have options that fit their unique situations.

The bottom line? A strong benefits strategy isn’t about offering more stuff. It’s about offering the right stuff: and making sure people understand what they have access to.

If you’re ready to explore how voluntary benefits can strengthen your package (without the headache), we’re here to help. No jargon. No pressure. Just straight talk about what works for you and your team.

Leave a comment